Analyzing the critical steps in deep learning-based stock forecasting: a literature review

- Published

- Accepted

- Received

- Academic Editor

- Marco Piangerelli

- Subject Areas

- Human-Computer Interaction, Artificial Intelligence, Data Mining and Machine Learning, Data Science, Neural Networks

- Keywords

- Deep learning, Stock forecasting, Feature selection, Feature extraction, Denoising, Sliding window, Trading simulation

- Copyright

- © 2024 Akşehir and Kılıç

- Licence

- This is an open access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, reproduction and adaptation in any medium and for any purpose provided that it is properly attributed. For attribution, the original author(s), title, publication source (PeerJ Computer Science) and either DOI or URL of the article must be cited.

- Cite this article

- 2024. Analyzing the critical steps in deep learning-based stock forecasting: a literature review. PeerJ Computer Science 10:e2312 https://doi.org/10.7717/peerj-cs.2312

Abstract

Stock market or individual stock forecasting poses a significant challenge due to the influence of uncertainty and dynamic conditions in financial markets. Traditional methods, such as fundamental and technical analysis, have been limited in coping with uncertainty. In recent years, this has led to a growing interest in using deep learning-based models for stock prediction. However, the accuracy and reliability of these models depend on correctly implementing a series of critical steps. These steps include data collection and analysis, feature extraction and selection, noise elimination, model selection and architecture determination, choice of training-test approach, and performance evaluation. This study systematically examined deep learning-based stock forecasting models in the literature, investigating the effects of these steps on the model’s forecasting performance. This review focused on the studies between 2020–2024, identifying influential studies by conducting a systematic literature search across three different databases. The identified studies regarding seven critical steps essential for creating successful and reliable prediction models were thoroughly examined. The findings from these examinations were summarized in tables, and the gaps in the literature were detailed. This systematic review not only provides a comprehensive understanding of current studies but also serves as a guide for future research.

Introduction

Stock forecasting is an interdisciplinary field aiming to forecast the future movements of asset prices in financial markets and represents the intersection between finance and computer science. The predictability of price movements in financial markets is an important topic of discussion within Fama’s random walk hypothesis (Fama, 1995). According to this hypothesis, market prices follow a random walk process, and current prices are independent of past price movements. However, recent research suggests that market prices are predictable in some cases.

In recent years, stock forecasting models have become more complex and data-driven with the advancement of computer technologies such as artificial intelligence, machine learning, deep learning, and big data analytics. These technologies enable the development of models that forecast future price movements by analyzing historical data. However, despite being supported by advanced technologies, stock forecasting inherently involves uncertainties due to the nature of financial markets. The underlying reasons for these uncertainties are company news, economic indicators, political events, investor psychology, etc. Consequently, all these factors directly affect the effectiveness of prediction models. Therefore, numerous studies have been conducted on the reliability and accuracy of stock forecasting models, and there are also numerous studies about them.

As a result of the research conducted, it has been determined that creating a successful model for stock forecasting involves some critical steps. These steps include data collection and analysis, feature extraction and selection, noise elimination, model selection, architecture adoption, approach selection for model training, and evaluation of model performance. The correct implementation of each of the steps detailed below plays an important role in creating a forecasting model that can make accurate forecasts and predict the future movements of financial assets. These steps and their details are as follows:

-

Data collection and analysis: When creating a successful model for stock forecasting, the first step is to collect and analyze data related to the stock item. These data include variables such as stock indices, stock prices, trading volumes, technical indicators, relevant news data, macroeconomic indicators, etc. The collection and analysis of these data form the basis of the prediction model and help understand future price movements. Accurate and comprehensive collection of stock market data is a critical factor determining the accuracy and effectiveness of the prediction model.

-

Feature extraction: Extracting meaningful features from stock data significantly impacts the prediction model’s performance. For example, extracting trends and seasonal patterns from financial time series data. These features can assist the model in predicting future price movements more accurately. Therefore, extracting appropriate features from stock data and utilizing them is vital in creating a successful prediction model.

-

Feature selection: There are typically numerous features associated with stock data, some of which may be unnecessary or ineffective. Therefore, identifying and removing unnecessary features is important in creating a successful prediction model. Feature selection reduces the complexity of the model and enables better learning by eliminating unnecessary information. Therefore, choosing a suitable feature is an important step for stock forecasting.

-

Noise elimination: Due to the influence of numerous factors, stock data often contains noise. This noise can adversely affect the performance of prediction models. Therefore, it is important to clean or reduce noise from stock data. This process can be performed using filtering methods, smoothing techniques, outlier detection, etc. Noise elimination is an important step in stock prediction because it increases the likelihood of models making more reliable predictions when working with accurate and clean datasets.

-

Model selection and architectural structure: Selecting an appropriate model and defining its architectural structure are fundamental steps in creating a successful forecasting model for stock prediction. At this stage, the deep learning technique to be utilized should be determined, and their performance on stock data should be evaluated. Additionally, determining the architectural structure of the chosen model is crucial. This architectural structure includes organizing the input and output layers of the model and its internal layers. Establishing the correct architectural structure enables the model to learn better and make more effective predictions on stock data.

-

Selection of training-test approach: The choice of the training-test approach directly affects the model’s prediction performance, and two primary methods are commonly preferred: the traditional train-test split and the sliding window approach. In the traditional method, a certain percentage of the dataset is used for training, while the remainder is reserved for testing. This method provides a quick and easy performance evaluation but may limit the model’s generalization ability and may not sufficiently account for changing market conditions. On the other hand, in the sliding window approach, training and test sets are created by sliding over a specified period. This method often yields more realistic results as it helps the model adapt to changing market conditions.

-

Performance evaluation: Evaluating the performance of the constructed prediction model is critical to understanding and improving its effectiveness. At this stage, the defined model architecture should undergo training and validation processes, and the model’s predictive ability should be measured. During this process, the differences between the values predicted by the model and the actual values are observed, and the model’s performance is evaluated using various evaluation metrics such as statistical metrics and trading simulation.

This study conducted a systematic literature review for deep learning-based trend and price prediction of both stock indices and individual stocks. Searches were performed across three different databases using predefined search queries to achieve this. Subsequently, studies were filtered based on exclusion and inclusion criteria applied to these searches. In the final stage, the identified studies were analyzed in detail based on the abovementioned criteria.

Motivation and contributions

Based on the literature review conducted for this study, it was noted that there is a lack of systematic evaluation encompassing all criteria related to data collection and analysis, feature extraction and selection, noise elimination, model selection, architecture adoption, approach selection for model training, and evaluation of model performance for both stock index and individual stock forecasting. To address this gap, review studies focusing on deep learning models were primarily explored. Six studies published in journals with Q1 or Q2 quarterly rankings between 2020 and 2024 were meticulously examined for this purpose. These review studies were evaluated based on the following eight criteria, and the results of this evaluation are given in Table 1.

| Review studies | C1 | C2 | C3 | C4 | C5 | C6 | C7 | C8 |

|---|---|---|---|---|---|---|---|---|

| Stock market forecasting using deep learning and technical analysis: A systematic review (Li & Bastos, 2020) | ✓ | X | ✓ | X | X | X | ✓ | ✓ |

| Stock market movement forecast: A systematic review (Bustos & Pomares-Quimbaya, 2020) | ✓ | X | ✓ | X | X | X | ✓ | ✓ |

| Decision fusion for stock market prediction: A systematic review (Zhang, Sjarif & Ibrahim, 2022) | ✓ | X | ✓ | X | X | X | ✓ | ✓ |

| An overview of machine learning, deep learning, and reinforcement learning-based techniques in quantitative finance: Recent progress and challenges (Sahu, Mokhade & Bokde, 2023) | X | X | ✓ | X | X | X | ✓ | ✓ |

| News-based intelligent prediction of financial markets using text mining and machine learning: A systematic literature review (Ashtiani & Raahemi, 2023) | ✓ | X | ✓ | X | X | X | ✓ | ✓ |

| A systematic literature survey on recent trends in stock market prediction (Balasubramanian et al., 2024) | X | X | ✓ | X | X | X | ✓ | ✓ |

| This study | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ |

-

C1: How was the search process carried out through databases for the studies to be examined in the review study? Has statistical information been provided about them? Therefore, is the review study systematic?

-

C2: Have the studies under consideration been summarized individually, with the suggested prediction models in these studies expressed in general terms, and has there been discussion about their contributions to the literature?

-

C3: Has a detailed investigation been conducted on the input features used in prediction models?

-

C4: Has information been given about the feature selection or extraction methods used for prediction models?

-

C5: Has the focus been on proposed approaches to removing noise or denoising in stock data?

-

C6: Has there been a detailed explanation of the different training-test approaches used in prediction models?

-

C7: Has information been provided regarding which type of deep learning methods the proposed prediction models in the studies have focused on?

-

C8: Have the metrics used to evaluate the performance of the proposed models been investigated?

As a result of the reviews, it has been observed that all six review studies focused on the input features and deep learning approaches used in prediction models, along with model performance evaluation. While most of the review studies were systematic, none focused on feature selection/extraction, noise reduction, and train-test approaches. It has been found that only detailed research conducted on input features, prediction methods, and model performance cannot guide more successful stock forecasting models.

Due to the chaotic nature of the data considered for the stock price prediction problem and its high noise level, applying various preprocessing steps is important and necessary. Especially, the successful implementation of these steps may positively affect the model’s overall performance. Also, noise reduction or denoising techniques can enhance the model’s learning accuracy by minimizing unwanted variance in the dataset. Similarly, feature selection or extraction processes can optimize learning by filtering out irrelevant information and focusing on the most relevant features.

Another important point is which of the traditional training-test split or sliding window approach will be used in the training phase of the model. It is important for the dataset to be appropriately divided and for the data used during the model training stage to reflect real-world conditions, as this directly impacts the model’s performance. Consequently, focusing solely on input features and prediction methods is insufficient for creating a successful stock prediction model. Applying appropriate preprocessing steps tailored to the data and using suitable evaluation techniques to improve model accuracy is necessary to obtain more reliable and effective predictions.

As a result of the literature research, it was noted that a systematic review study focusing on all criteria related to data collection and analysis, feature extraction and selection, noise elimination, model selection, architecture adoption, approach selection for model training, and evaluation of model performance for creating a successful deep learning-based stock forecasting model had not been conducted. This situation constitutes our main motivation. To address this gap in the literature, this study conducted a systematic review of deep learning-based stock prediction studies between 2020 and 2024, evaluating each study based on the eight criteria listed above. Therefore, this constitutes the main contribution of this study. Additionally, we believe that this study will shed light on researchers working on stock forecasting problems.

The audience it is intended for

The intended readership of this study comprises scholars, researchers, and professionals engaged in the interdisciplinary domains of finance, computational finance, machine learning, and artificial intelligence. Primarily, this research targets academics and researchers interested in applying deep learning methodologies in financial time series analysis and forecasting. Furthermore, practitioners involved in quantitative finance, algorithmic trading, and investment management will find the insights gleaned from this study invaluable for refining their predictive modeling strategies. Additionally, graduate students and postdoctoral researchers conducting research in financial data analysis and predictive modeling may benefit from the comprehensive review and analysis presented herein. In summary, this study addresses a scholarly audience interested in advancing the understanding and application of deep learning approaches in financial forecasting.

Organization

The rest of the study is organized as follows: In the ‘Research Methodology’ section, the selection process for the studies examined in the review is detailed. The ‘Obtained Findings and Results’ section begins with a detailed summary of these studies, followed by a comprehensive examination within the scope of the identified research questions. The ‘Conclusion and Recommendations’ section provides a general evaluation of the examined studies and offers recommendations for future research.

Research Methodology

This systematic review study begins with a process of defining research questions, focusing on the identified objectives. Then, database scans are performed to select studies that will provide the necessary information to answer these research questions. These scans are performed on the query sentences determined based on predefined criteria. Finally, the examination and elimination process of the studies obtained from the database searches is carried out. This process includes the evaluation of the suitability of the studies to the determined criteria and their contribution to the review objectives. Thus, in-depth research is provided by systematically evaluating the information in the literature, and the basis for future research is created.

Research strategy

This systematic review study aims to achieve the identified goal by addressing the following research questions:

-

RQ1: Which deep learning methods are preferred in stock prediction models?

-

RQ2: Which input features do the proposed prediction models focus on?

-

RQ3: How often are feature extraction-selection methods used in prediction models, and what is their impact on model performance?

-

RQ4: What methods are proposed for denoising stock data, and how often are they preferred?

-

RQ5: Which approach, sliding window or traditional train-test splitting, is more commonly preferred in prediction models?

-

RQ6: What metrics are used to evaluate the performance of models?

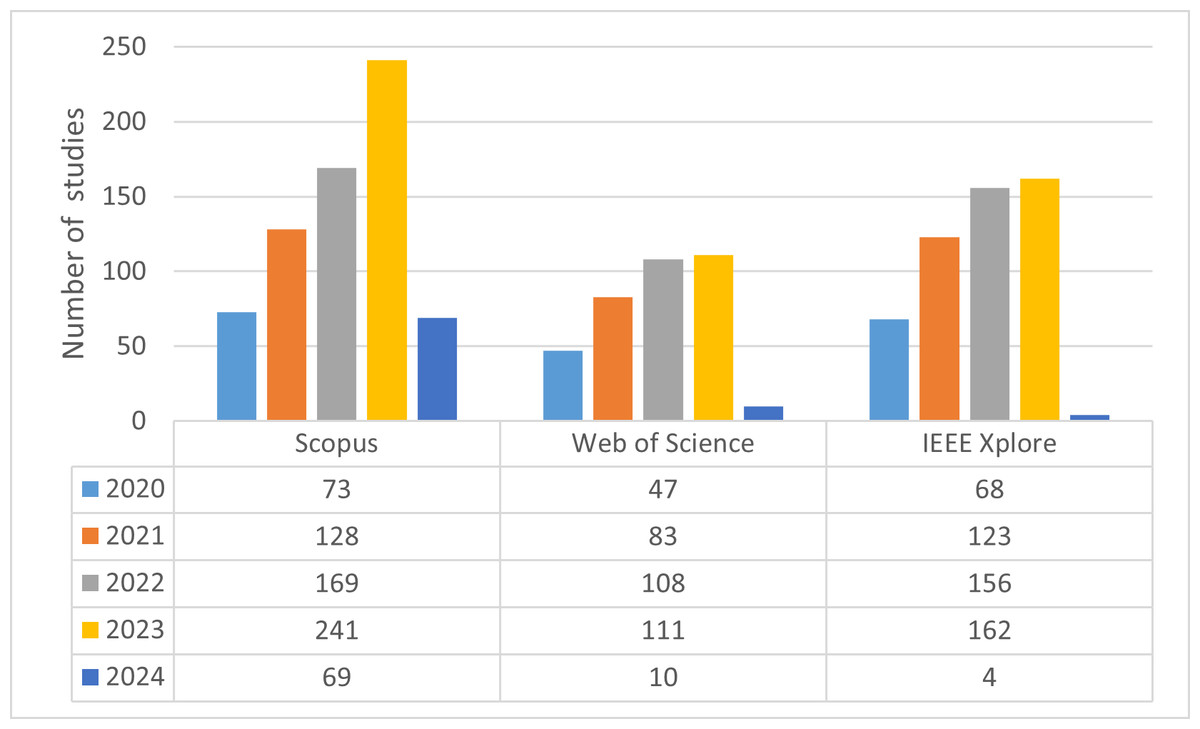

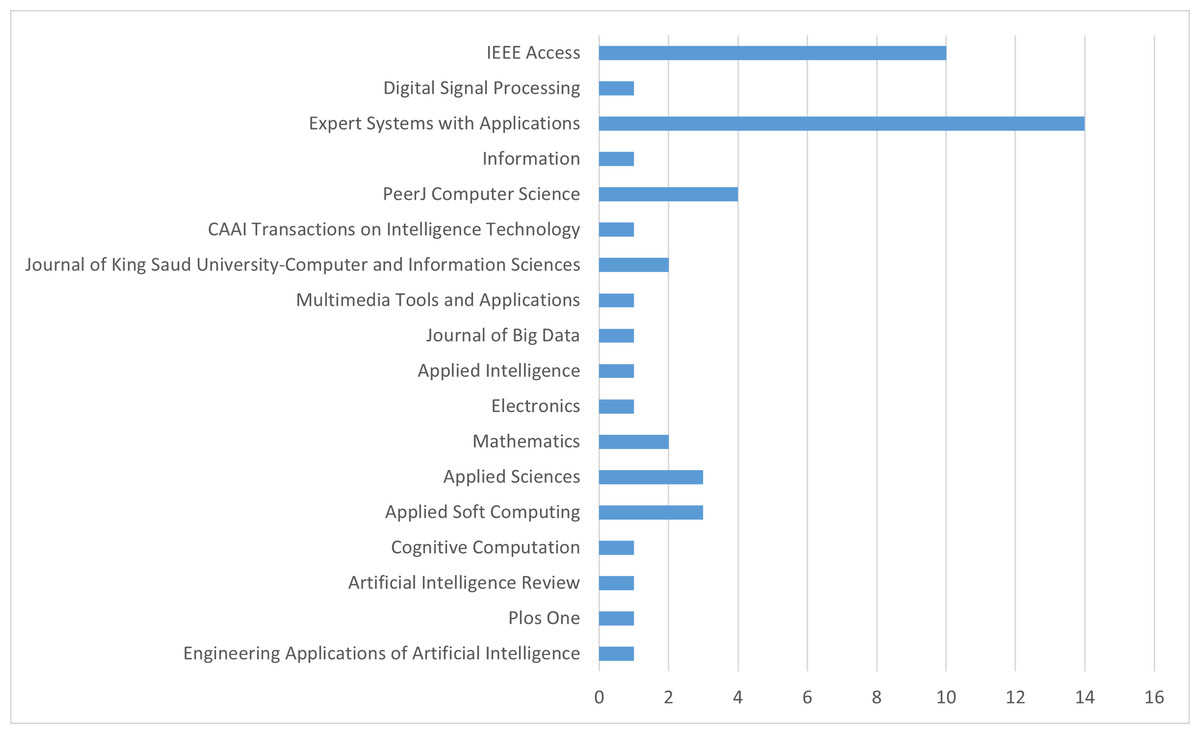

After determining the research questions, literature searches were conducted on four different databases: IEEE Xplore, Scopus, Web of Science, and Google Scholar. The search space was expanded using the “AND” operator for different keywords and the “OR” operator for synonyms of keywords. The query sentences used in this process and information about where they were searched are summarized in Table 2. Based on the information in the table, queries were conducted on the four databases. It has been determined that effective filtering cannot be performed on Google Scholar because queries on this database yield very general results as well as targeted studies. Therefore, Google Scholar searches were disregarded. As a result, the number of studies obtained from searches conducted on three different databases from 2020 to the present is summarized in Fig. 1, and a total of 1,552 studies were filtered through these searches.

| Database | Query statement |

|---|---|

| IEEE Xplore | ((“stock” OR “financial time serie” OR “financial”) AND (“forecast” OR “predict” )) AND (“deep learning” OR “DL”) |

| Scopus | (TITLE-ABS-KEY (((“stock” OR “financial time serie” OR “financial”) AND (“forecast” OR “predict” )) AND (“deep learning” OR “DL”))) |

| Web of Science | AB = (((“stock” OR “financial time serie” OR “financial”) AND (“forecast” OR “predict”)) AND (“deep learning” OR “DL”))) |

Figure 1: Number of filtered studies with query sentences in databases.

{kind=link}

Study selection

Some of the 1,552 studies obtained through the queries were found to be searched in multiple databases. Therefore, duplicates were removed to ensure that studies searched in databases were listed only once. In addition, the criteria for elimination and selection for determining whether the listed studies are worth examining within the scope of the review study were defined as follows:

-

Selection Criteria

-

Studies published between 2020 and 2024

-

Studies published in Q1(top 25% journals with the highest impact factor) or Q2 (journals in the 25–50% impact factor range) quarterly computer science journals

-

Studies focusing on either stock index or individual stock forecasting

-

Studies written in English

-

-

Elimination Criteria

-

Studies not focusing on deep learning methods for stock forecasting

-

Studies being either review articles or conference papers

-

Studies focusing on exchange rate forecasting, portfolio optimization, gold price forecasting, financial risk assessment, etc.

-

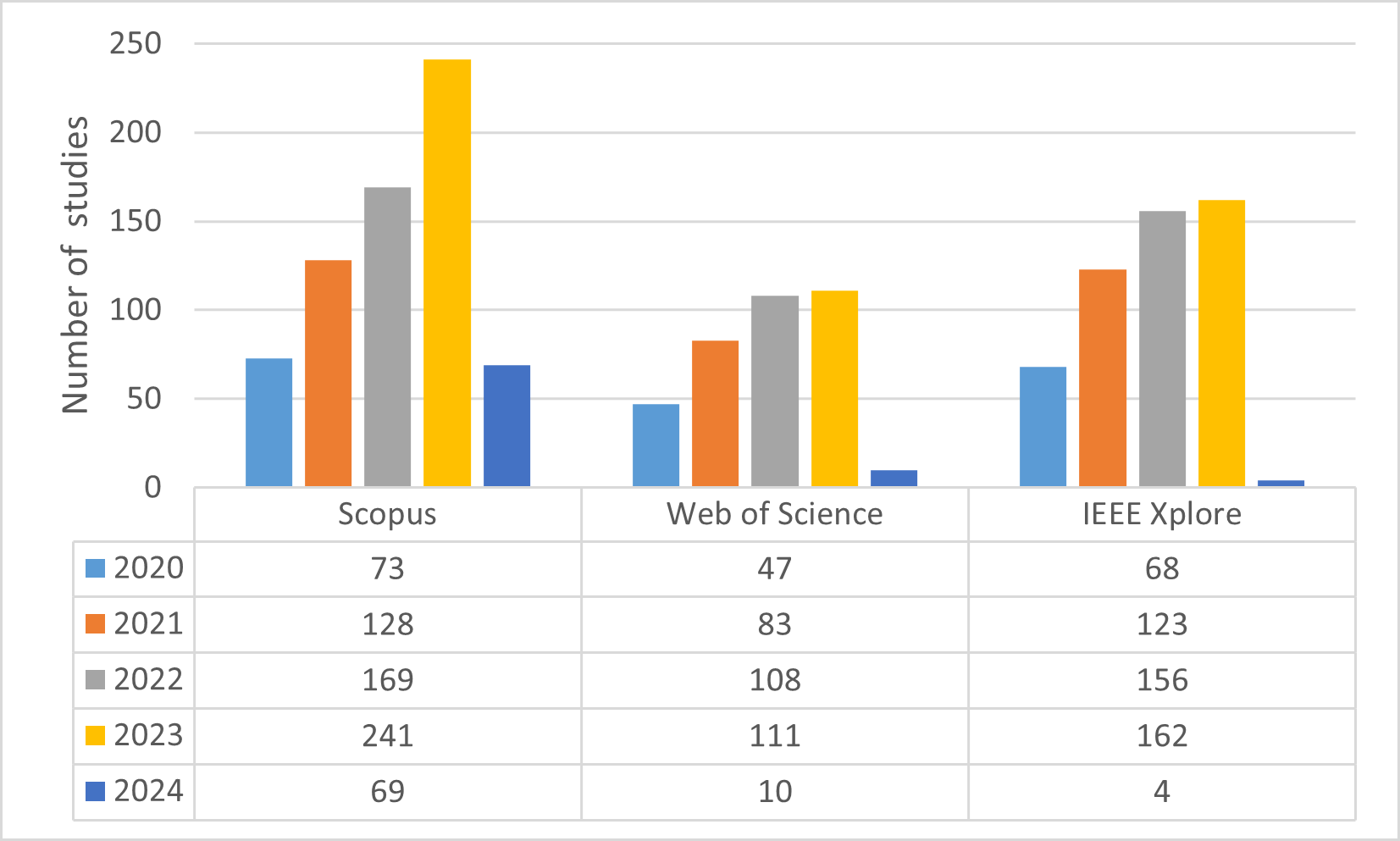

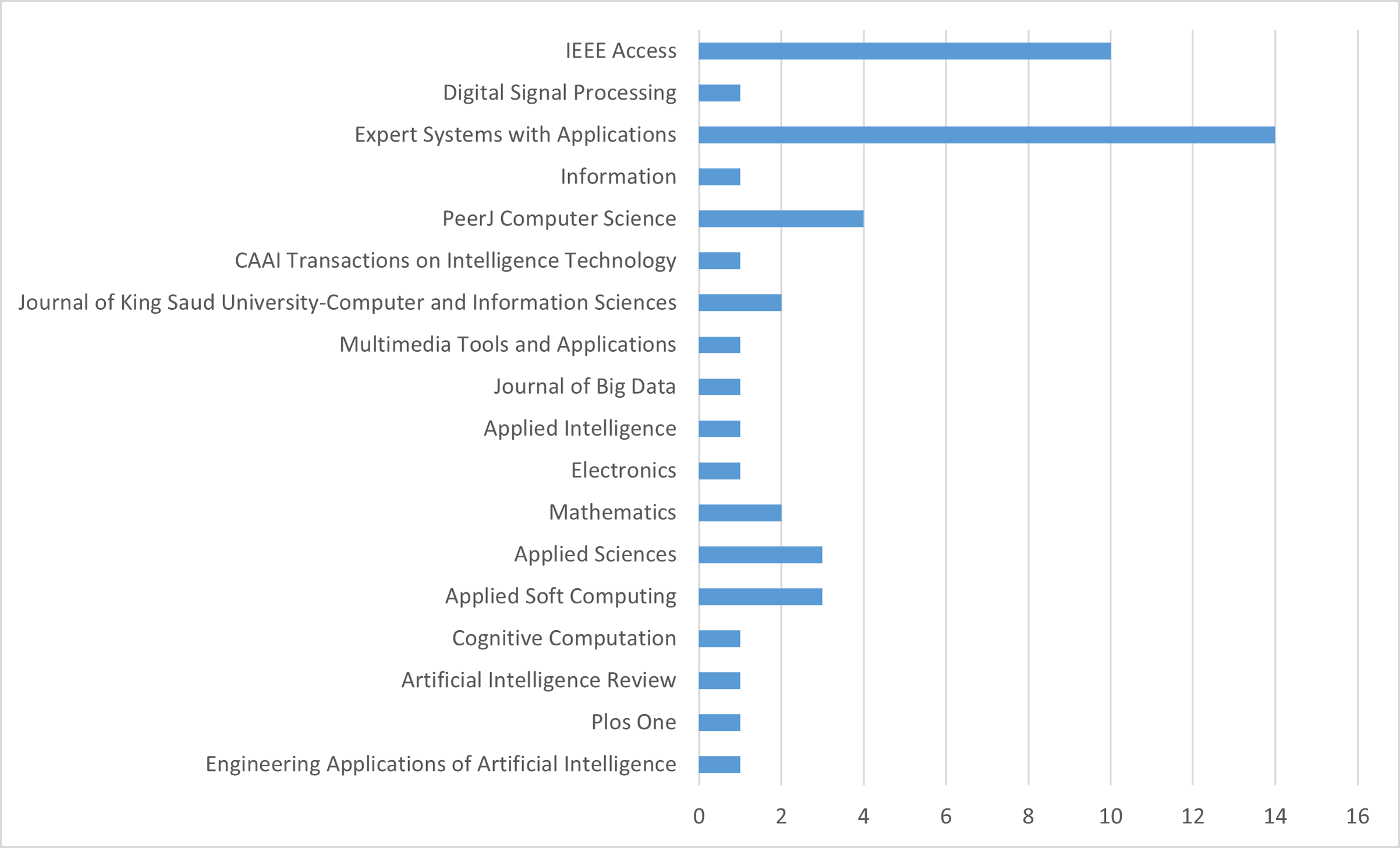

The titles and abstracts of the studies were read, and out of the 1,552 studies identified based on the criteria mentioned above, 49 have been selected and listed in Table 3. These studies include 25 open-access articles. Additionally, an analysis of the journals in which these selected studies were published is provided in Fig. 2. According to this analysis, it is observed that the majority of the selected studies were published in Expert Systems With Applications and IEEE Access journals.

| Title of paper | Publication year |

Open access |

|---|---|---|

| Stock Prediction Based on Genetic Algorithm Feature Selection and Long Short-Term Memory Neural Network (Chen & Zhou, 2020) | 2020 | ✓ |

| Forecasting Stock Prices Using a Hybrid Deep Learning Model Integrating Attention Mechanism, Multi-Layer Perceptron, and Bidirectional Long-Short Term Memory Neural Network (Chen, Zhang & Lou, 2020) | 2020 | ✓ |

| An Efficient Word Embedding and Deep Learning Based Model to Forecast the Direction of Stock Exchange Market Using Twitter and Financial News Sites: A Case of Istanbul Stock Exchange (BIST 100) (Kilimci & Duvar, 2020) | 2020 | ✓ |

| An Improved Deep Learning Model for Predicting Stock Market Price Time Series (Liu & Long, 2020) | 2020 | X |

| Stock Trend Prediction using Candlestick Charting and Ensemble Machine Learning Techniques with A Novelty Feature Engineering Scheme (Lin et al., 2021) | 2021 | ✓ |

| A Novel Improved Particle Swarm Optimization With Long-Short Term Memory Hybrid Model for Stock Indices Forecast (Ji, Liew & Yang, 2021) | 2021 | ✓ |

| Combining Deep Learning and Multiresolution Analysis for Stock Market Forecasting (Althelaya, Mohammed & El-Alfy, 2021) | 2021 | ✓ |

| Forecasting Stock Market Indices Using Padding-Based Fourier Transform Denoising and Time Series Deep Learning Models (Song, Baek & Kim, 2021) | 2021 | ✓ |

| Stock Market Index Prediction Based on Reservoir Computing Models (Wang et al., 2021) | 2021 | X |

| Predicting Stock Movements: Using Multiresolution Wavelet Reconstruction and Deep Learning in Neural Networks (Peng, Chen & Li, 2021) | 2021 | ✓ |

| Explainable Stock Prices Prediction From Financial News Articles Using Sentiment Analysis (Gite et al., 2021) | 2021 | X |

| LSTM-Based Sentiment Analysis for Stock Price Forecast (Ko & Chang, 2021) | 2021 | ✓ |

| Stock Values Predictions Using Deep Learning Based Hybrid Models (Yadav, Yadav & Saini, 2022) | 2022 | ✓ |

| Knowledge Graph and Deep Learning Combined With a Stock Price Prediction Network Focusing on Related Stocks and Mutation Points (Tao et al., 2022) | 2022 | ✓ |

| Stock Market Index Prediction Using Deep Transformer Model (Wang et al., 2022) | 2022 | X |

| Modal Decomposition-Based Hybrid Model for Stock Index Prediction (Lv et al., 2022) | 2022 | X |

| A Stock Market Trading Framework Based on Deep Learning Architectures (Shah et al., 2022) | 2022 | X |

| Implementation of Long Short- Term Memory and Gated Recurrent Units on Grouped Time- Series Data to Predict Stock Prices Accurately (Lawi, Mesra & Amir, 2022) | 2022 | ✓ |

| China’s Commercial Bank Stock Price Prediction Using a Novel K-means-LSTM Hybrid Approach (Chen, Wu & Wu, 2022) | 2022 | X |

| AEI-DNET: A Novel DenseNet Model with an Autoencoder for the Stock Market Predictions Using Stock Technical Indicators (Albahli et al., 2022) | 2022 | ✓ |

| StockNet—GRU Based Stock Index Prediction (Gupta, Bhattacharjee & Bishnu, 2022) | 2022 | X |

| Multi-Model Generative Adversarial Network Hybrid Prediction Algorithm (MMGAN-HPA) for Stock Market Prices Prediction (Polamuri, Srinivas & Mohan, 2022) | 2022 | ✓ |

| How to Handle Data Imbalance and Feature Selection Problems in CNN-based Stock Price Forecasting (Akşehir & Kiliç, 2022) | 2022 | ✓ |

| Instance-Based Deep Transfer Learning with Attention for Stock Movement Prediction (He, Siu & Si, 2023) | 2023 | X |

| Integrating Piecewise Linear Representation and Deep Learning for Trading Signals Forecasting (Chen & Zhu, 2023) | 2023 | ✓ |

| Stock Price Prediction Model Based on Investor Sentiment and Optimized Deep Learning (Mu et al., 2023) | 2023 | ✓ |

| Stock Price Prediction Using CNN-BiLSTM-Attention Model (Zhang, Ye & Lai, 2023) | 2023 | ✓ |

| Shortlisting Machine Learning-Based Stock Trading Recommendations Using Candlestick Pattern Recognition (Cagliero, Fior & Garza, 2023) | 2023 | X |

| Combining CNN and Grad-CAM for Profitability and Explainability of Investment Strategy: Application to The KOSPI 200 Futures (Kim et al., 2023) | 2023 | X |

| GRU Neural Network Based on CEEMDAN–Wavelet for Stock Price Prediction (Qi, Ren & Su, 2023) | 2023 | ✓ |

| Stock Index Forecasting Based on Multivariate Empirical Mode Decomposition and Temporal Convolutional Networks (Yao, Zhang & Zhao, 2023) | 2023 | X |

| Deep Learning-based Integrated Framework for Stock Price Movement Prediction (Zhao & Yang, 2023) | 2023 | X |

| Predicting Saudi Stock Market Index by Using Multivariate Time Series Based on Deep Learning (Jarrah & Derbali, 2023) | 2023 | ✓ |

| A Multi- Factor Two- Stage Deep Integration Model for Stock Price Prediction Based on Intelligent Optimization and Feature Clustering (Wang & Zhu, 2023a) | 2023 | X |

| Novel Optimization Approach for Stock Price Forecasting Using Multi-Layered Sequential LSTM (Md et al., 2023) | 2023 | X |

| A Multi-Parameter Forecasting for Stock Time Series Data Using LSTM and Deep Learning Model (Zaheer et al., 2023) | 2023 | ✓ |

| A Novel Stock Index Direction Prediction Based on Dual Classifier Coupling and Investor Sentiment Analysis (Wang & Zhu, 2023b) | 2023 | X |

| A Comparative Study on Effect of News Sentiment on Stock Price Prediction with Deep Learning Architecture (Dahal et al., 2023) | 2023 | ✓ |

| Novel Optimization Approach for Realized Volatility Forecast of Stock Price Index Based on Deep Reinforcement Learning Model (Yu et al., 2023) | 2023 | X |

| An Improved DenseNet Model for Prediction of Stock Market Using Stock Technical Indicators (Albahli et al., 2023) | 2023 | X |

| Movement Forecasting of Financial Time Series Based on Adaptive LSTM-BN Network (Fang et al., 2023) | 2023 | X |

| Forecasting Stock Market Indices Using the Recurrent Neural Network Based Hybrid Models- CNN-LSTM, GRU-CNN, and Ensemble Models (Song & Choi, 2023) | 2023 | ✓ |

| McVCsB: A New Hybrid Deep Learning Network for Stock Index Prediction (Cui et al., 2023) | 2023 | X |

| Neural Network Systems With an Integrated Coefficient of Variation-Based Feature Selection for Stock Price and Trend Prediction (Chaudhari & Thakkar, 2023) | 2023 | X |

| Forecasting Multistep Daily Stock Prices for Long-Term Investment Decisions: A Study of Deep Learning Models on Global Indices (Beniwal, Singh & Kumar, 2024) | 2024 | X |

| An Enhanced Interval-Valued Decomposition Integration Model for Stock Price Prediction Based on Comprehensive Feature Extraction and Optimized Deep Learning (Wang, Liu & Jiang, 2024) | 2024 | X |

| A New Denoising Approach Based on Mode Decomposition Applied to The Stock Market Time Series: 2LE-CEEMDAN (Akşehir & Kılıç, 2024b) | 2024 | ✓ |

| Multi Level Perspectives in Stock Price Forecasting: ICE2DE-MDL (Akşehir & Kılıç, 2024a) | 2024 | ✓ |

| A Novel Hierarchical Feature Selection with Local Shuffling and Models Reweighting for Stock Price Forecasting (An et al., 2024) | 2024 | X |

Obtained Findings and Results

Each of the 49 studies is first summarized in detail in this section, and the prediction models proposed in the studies are explained. This allows researchers to have comprehensive information about each study, compare studies, and fill the gaps in the literature. Following that, the studies have been individually analyzed for each research question.

Study summaries

Chen & Zhou (2020) pointed out in their study that many factors affect stock prices and emphasized that the factors influencing each stock may vary. They suggested that instead of considering all factors in stock prediction models, focusing on the most important factors influencing each stock is necessary. In this context, they proposed a long short term memory (LSTM)-based forecasting framework that utilizes genetic algorithm (GA) to determine and optimize multiple factor combinations for predicting stock prices. The proposed GA-LSTM prediction model considered 40 factors consisting of technical indicators and financial factors affecting stocks, and GA was used to obtain the importance ranking of these factors. Accordingly, five feature sets were created, including top 30, 20, 10, five, and all factors. The LSTM model was trained using these feature sets, and the optimal factor combination was determined according to the findings. The proposed GA-LSTM prediction model was applied to the China Construction Bank and CSI 300 stock datasets. When the experimental results were evaluated, it was seen that higher prediction performance was achieved with feature sets consisting of the top 10 factors for the China construction bank dataset and the top 20 factors for the CSI 300 stock dataset. Therefore, this study underscores the importance of GA for multi-factor modeling in the stock market and demonstrates its positive impact on more accurate prediction of stock prices.

Chen, Zhang & Lou (2020) proposed a novel hybrid prediction model consisting of an attention mechanism, multi-layer perceptron (MLP), and bidirectional LSTM (BiLSTM) for stock index forecasting. For this proposed model, data from four different sources were combined, including price data from stock indices, technical indicators, historical data from the Google index, and prices of natural resources such as gold, silver, and oil. Accordingly, a total of 45 features were obtained for each stock index. Before moving on to the training phase, feature selection and dimension reduction were performed on these features. Initially, Pearson correlation analysis was conducted on the identified 27 technical indicators, selecting the most important 14 technical indicators. Subsequently, dimension reduction using principal component analysis (PCA) was performed on 31 features. Therefore, as a result of all these processes, the raw data containing four different data sets was transformed into a knowledge base. Then, this dataset was fed into a network consisting of MLP, BiLSTM, and attention mechanisms for predicting the closing values of stock indices. In this network architecture, MLP was used for fast convergence of the algorithm, BiLSTM for extracting temporal features of index data, and the attention mechanism to focus more on crucial temporal information of the neural network. The proposed model was used to predict the closing values of the S&P 500, Russell 2000, NASDAQ, and Dow Jones stock indices, and its prediction performance was compared with seven different prediction models. Experimental results indicated that the proposed model outperformed other prediction models, particularly emphasizing the significant success of the attention mechanism in stock forecasting.

Figure 2: Ranking of journals.

{kind=link}

Kilimci & Duvar (2020) focused on financial sentiment analysis using Turkish datasets, unlike recent studies aimed at predicting the stock market’s direction. Their analysis was based on nine high-volume bank stocks from the Istanbul Stock Exchange (BIST 100). They proposed a prediction model based on word embedding and deep learning techniques. They stated that while English news texts have been used for stock market direction prediction, combining deep learning techniques and word embedding methods has yet to be used to predict the direction of Turkish stocks and markets. Accordingly, individual comments and news texts from various sources such as Twitter, KAP, Mynet Finans, and Bigpara were collected. After collecting and cleaning the datasets, nine prediction models were proposed by combining Word2Vec, GloVe, and FastTex word embedding techniques with recurrent neural network (RNN), LSTM, and convolutional neural network (CNN) deep learning approaches to predict the direction of BIST 100. When evaluating the classification performance of the proposed models, it was observed that the combination of FastText and LSTM generally made successful predictions, and RNN and LSTM methods outperformed CNN in all datasets. Therefore, this study shows that combining word embedding techniques and deep learning models provides an important analytical tool for investors.

Liu & Long (2020) proposed a hybrid forecasting framework for daily closing price prediction of stock market indices. The proposed EWT-dpLSTM-PSO-ORELM prediction model combined empirical wavelet transform (EWT) based decomposition, dropout strategy, particle swarm optimization (PSO) based LSTM deep network optimization, and outlier robust extreme learning machine (ORELM) based error correction methods. Three different datasets were used to demonstrate the proposed model’s effectiveness: the S&P 500 Index, China Minsheng Bank (CMSB), and the Dow Jones Industrial Average (DJI). Approximately three years of historical price data were collected for these data sets, and the first two years of this data were used in the model’s training, and the remaining one year was used in the testing. To evaluate the prediction performance of the proposed model, it was compared with three different prediction models from the literature using traditional backpropagation neural network (BPNN), random forest (RF), and single LSTM methods. Additionally, to investigate the impact of each module in the proposed model on prediction performance, a total of seven models were created: dpLSTM, dpLSTM-PSO, EWT-dpLSTM-PSO, dpLSTM-PSO-ORELM, dpLSTM-PSO-RELM, dpLSTM-PSO-WRELM, and dpLSTM-PSO-ELM. All these prediction models were applied to each dataset, and the closing prices of stock indices for the next day were predicted. The comparisons showed that the EWT-dpLSTM-PSO-ORELM model outperformed the BPNN, RF, and single LSTM-based prediction models for all three datasets. Therefore, it was proven that the proposed hybrid model achieved more accurate prediction results than single models based on machine learning or deep learning methods. Furthermore, comparisons with the other seven models revealed that applying the EWT algorithm resulted in the decomposition of complex stock closing prices into stable sub-layers, and the combination of ORELM error correction with EWT decomposition methods significantly improved prediction accuracy. The experiments also showed that the integrated decomposition and error correction model had higher prediction accuracy. At the same time, the dropout strategy and PSO algorithm enhanced the prediction performance of the LSTM network. Thus, the experimental results demonstrated that the proposed EWT-dpLSTM-PSO-ORELM prediction model outperformed other deep learning methods or single models in terms of prediction accuracy. Additionally, it was expressed as future work that this proposed prediction framework would be applied to other financial time series predictions.

Lin et al. (2021) combined traditional candlestick chart analysis with machine learning methods such as logistic regression, support vector machine (SVM), K-nearest neighbors (KNN), RF, gradient boosting decision tree (GBDT), and LSTM for stock prediction. In the study, an eight-trigram classification scheme was developed in feature engineering, and the importance of various technical indicators was thoroughly examined for short-term stock prediction. Additionally, an innovative feature engineering scheme compatible with a machine learning method selection framework was proposed to automatically select the most suitable machine learning method for different candlestick charting patterns. The proposed prediction framework was applied to all stocks in the China stock market. Accordingly, daily stock data for 18 years (between 2000 and 2017) were collected. Then, a feature set was created for each trading day, including the date, intra-day pattern, inter-day pattern, 21 technical indicators, and the next day’s closing price. To examine the effect of technical indicators in the proposed forecast model, these indicators were discussed under four groups: overlap, momentum, volume, and volatility. Thus, six different feature sets, including without indicators, with all indicators, volume indicators, overlap indicators, momentum indicators, and volatility indicators, were applied with six machine learning methods. When the results obtained were evaluated, it was observed that RF and GBDT generally had a good forecasting ability in short-term forecasts, but LSTM performed worse than other methods in this scenario. It has also been stated that using fewer momentum and volatility indicators in short-term forecasts increases forecast performance to a satisfactory level. Finally, an investment strategy based on forecasting frameworks was developed, and experimental results confirmed that this strategy could provide significant economic returns on individual stocks and portfolios.

Ji, Liew & Yang (2021) proposed a hybrid model consisting of improved particle swarm optimization (IPSO) and LSTM for predicting stock market indices. It has been stated that when the standard PSO algorithm is used for hyperparameter optimization of the LSTM network, rapid convergence to the local optimum occurs, negatively affecting the prediction performance. In response to this issue, they proposed the IPSO method based on a new inertia weight and adaptive mutation factor for more effective hyperparameter optimization. The performance of the proposed model was evaluated using four different performance metrics on five stock market indices: Australian Stock Market (ASM), DJI, IXIC, Hang Seng Index (HSI), and Nikkei 225. For the experiments, 10-year daily historical data of stock market indices were used. Additionally, the performance of the proposed IPSO-LSTM model was compared with support vector regression (SVR), LSTM, and PSO-LSTM models. The comparative analysis demonstrates that the proposed IPSO-LSTM model performs best and exhibits successful generalization ability across different market indices.

Althelaya, Mohammed & El-Alfy (2021) proposed an innovative financial time series prediction approach, combining multiresolution analysis and the LSTM. The study investigated the effect of stationary wavelet transform (SWT) and EWT multiresolution analysis methods on predicting the S&P 500 index. To this end, approximately eight years of data from January 1, 2010, to February 20, 2018, for both long-term (30 days ahead) and short-term (next day) predictions of the S&P 500 index were collected from Yahoo Finance. The proposed hybrid model consists of three stages: in the first stage, financial time series data was decomposed using multiresolution analysis. Then, a separate LSTM network was trained for each resolution level. Finally, the final target value was estimated by combining the obtained estimates. Experimental results demonstrate that EWT outperformed SWT for both long-term and short-term predictions of the S&P 500. The results indicate that better patterns were obtained with EWT, suggesting the potential for creating more effective prediction models.

Song, Baek & Kim (2021) highlighted that noise in financial time series data impedes the learning of prediction models and causes time delays. To address this issue, they proposed a padding-based Fourier transformation denoising approach (P-FTD) to eliminate noise and resolve the data delay problem when reverting the time series to its original form. Hybrid prediction models, including P-FTD_RNN, P-FTD_LSTM, and P-FTD_GRU, which combine deep learning methods with P-FTD. These models were designed to predict the closing prices of S&P 500, SSE, and KOSPI stock indices. The performance of the proposed models was compared with basic gated recurrent unit (GRU), LSTM, and RNN models that did not utilize the denoising approach. Additionally, the effectiveness of the P-FTD approach was validated by comparing it with other denoising methods used in stock prediction models in the literature. Experimental results demonstrated that the hybrid models based on P-FTD outperformed the basic models in terms of prediction accuracy and also reduced time delays more effectively compared to other denoising methods.

Wang et al. (2021) emphasized the importance of using innovative deep-learning methods to predict price movements in financial markets. They researched the applicability of the reservoir computing (RC) method for predicting the daily closing price of stock indices. RC, a specialized type of RNN model, differs from traditional deep learning methods in that it only trains the weights of the output layer instead of all weights, significantly simplifying the training process. The primary motivation of Wang et al. (2021) in this study was the successful application of RC in time series prediction problems due to its nonlinear structure. However, it has not yet been applied to financial time series. To this end, RC prediction models were developed using three different network structures: random network, small-world network, and scale-free network. The proposed model predicted the closing price of seven stock indices, specifically S&P 500, NYSE, DJI, NASDAQ, FTSE 100, Nikkei 225, SSE for the next day. The proposed model’s prediction performance was evaluated in terms of statistical metrics (mean squared error (MSE), mean absolute error (MAE), R2, root mean square error (RMSE), mean absolute percentage error (MAPE)) and compared with four different predictions, including LSTM and RNN. The results indicated that the RC model generally exhibited competitive performance compared to leading models like LSTM and RNN, demonstrating its potential as a successful alternative for stock index prediction. However, some limitations of the model were also highlighted. Firstly, the study only covered seven stock indices, which could hinder the generalization of prediction models. Secondly, the dataset used only included daily closing prices, and the model’s performance was not evaluated on shorter time intervals (e.g., 1 h, 1 min). Lastly, the proposed model was not evaluated based on trading strategies developed for real-world applications. These limitations were identified as potential research areas for the broader evaluation and development of the RC model.

Peng, Chen & Li (2021) stated the significance of predicting the direction of stock prices in financial markets, highlighting it as a complex and challenging problem. To overcome this problem, they proposed combining wavelet analysis and deep learning methods to develop a prediction model. In the developed model, deep neural network (DNN) was chosen as the deep learning method, and db4 was selected as the wavelet function. To evaluate the effectiveness of the proposed model, medium-term (11 days) stock movement prediction was conducted using stock data from 168 US companies. Additionally, the performance of the proposed model was compared with machine learning methods such as Bayesian, RF, and artificial neural networks (ANN). The results indicated that this prediction model achieved an average accuracy rate of 75%, with particularly high accuracy rates achieved for some stocks such as Alibaba Group Holding and Toyota Motor. Comparative analyses showed that the deep learning method provided more stable and reliable predictions than other machine learning algorithms. Therefore, the primary contribution of this study was emphasized to be the effectiveness of deep learning and wavelet analysis methods in medium-term stock direction prediction. It has been stated that future studies aim to delve deeper into trading strategies and further examine the impact of financial indicators in detail.

Gite et al. (2021) emphasized the complexity of the stock market influenced by positive and negative sentiments in media news and proposed an effective model for predicting stock opening prices. This proposed model combines sentiment analysis based on news headlines with deep learning methods, incorporating the interpretability power of explainable artificial intelligence (XAI). Financial news headlines were collected from Pulse, allowing compilation of financial news, while Indian Stock Markets price data was obtained from Yahoo Finance. Two different models were developed for predicting stock opening prices. In the first model, only price data (open, high, low, close) was used as input, and LSTM was employed as the method. In the second model, sentiment analysis was performed on news headlines to determine whether each headline had a negative or positive sentiment. Then, this headline data was combined with price data and fed as input to the LSTM-CNN model. When evaluating the performance of the proposed two models, it was observed that the LSTM model achieved an accuracy of 88.73%, and the LSTM-CNN model achieved the same accuracy of 74.76%. Consequently, it was determined that the combination of LSTM and XAI provided higher accuracy than other models. It is stated that in future studies, research will be conducted on automatic predictions from news headlines on financial websites.

Ko & Chang (2021) proposed a hybrid model based on sentiment analysis and deep learning methods to predict the opening price of six stocks on the Taiwan Stock Exchange. They used three different categories of data for their proposed model. The first category consisted of daily transaction data of stocks, including information on opening, closing, high and low prices, and volume. The other two categories were textual data from news and forum posts. For the proposed model, first of all, sentiment analysis was performed separately on news and forum post data using the bidirectional encoder representations from transformers (BERT) method. This sentiment analysis obtained the textual data’s class (positive or negative) and probability information. Then, a total of four features were obtained for each type of data. A dataset was created using nine features obtained from textual and historical price data, and an LSTM model was trained on this dataset. Additionally, three different feature sets were created, including the feature set of historical price data, the feature set of news, and the feature set of forum posts. The experimental results showed that the sentiment analysis features of news or forum posts improved the model’s prediction performance. The LSTMNF model, which utilized all three data types, exhibited superior performance compared to the other three models. These results demonstrate the significant role of emotions in news and forums in the stock market. The authors also suggested that considering different types of sentiments would positively contribute to the model’s prediction performance and expressed their intention to conduct further studies.

Yadav, Yadav & Saini (2022) proposed two different deep learning-based models aimed at achieving more accurate and faster prediction of high-frequency and rapidly fluctuating stock prices. In the first proposed model, the FastRNN (Kusupati et al., 2018) method based on the ResNet architecture developed by Microsoft in 2018 was used to predict stock prices quickly. The aim was to achieve reasonable prediction accuracy with lower computational costs by leveraging FastRNN. In the second model, in addition to FastRNN, CNN and BiLSTM methods were employed to enhance prediction accuracy further. This model aimed to capitalize on the advantages of FastRNN to achieve higher prediction accuracy. The proposed models were applied to minute data of Facebook, Uber, Apple, and Nike stocks traded on the New York Stock Exchange. The performance of the models was evaluated in terms of both execution time and RMSE error metric and compared with four basic prediction models such as autoregresive integrated moving average (ARIMA), LSTM, FBProphet and CNN-LSTM. Experimental results demonstrated that the proposed models improved prediction accuracy and enhanced computational speed compared to other prediction models. This suggests that the proposed models could benefit investors, especially in livestock price prediction.

Tao et al. (2022) stated that numerous factors influence the stock market, yet many studies in the literature do not consider the interactions between stocks and sudden change points. In this direction, they proposed a deep learning-based hybrid model focusing on the relationship between stocks and change points. This proposed hybrid model consists of three sub-networks, each obtaining different features related to the stock. Subsequently, these features are merged to predict the stock’s closing price. The details of these sub-networks are provided as follows:

-

In the first sub-network, the historical price data of the stock is given as input to the ConvLSTM model, which is obtained by combining the LSTM model with the convolution structure, and the features are obtained.

-

The second sub-network utilizes the same architecture as the first one, but the input data differs. Here, a knowledge graph is used to explore the relationship between stocks, and based on this graph, a market information vector is obtained. This vector is then fed into the ConvLSTM model.

-

In the third sub-network, sudden changes in stock prices are considered. First, sudden change points are identified, and then a weight matrix is created based on the distance of each trading day to these change points. The motivation behind creating such a matrix is that “the shorter the distance, the greater the impact of the change point”. This matrix data is fed into the graph convolutional network (GCN) model to extract features.

Additionally, the model faces significant errors during training due to these sudden change points in stock price data. To address this issue, a piecewise loss function was proposed. This proposed hybrid forecasting framework was applied to four stocks in the Chinese market. Experimental results showed that the proposed model outperformed all other models for all four stocks, with the ConvLSTM model providing the closest prediction to the proposed model.

Wang et al. (2022) investigated the effectiveness of the transformer model, one of the deep learning methods, in forecasting stock market indices. Several important factors explain why they chose the transformer model as their focus. Firstly, the transformer model has achieved significant success in natural language processing, demonstrating its effectiveness in processing textual data. Secondly, the multi-head attention mechanism of the transformer is effective in emphasizing specific features and identifying important relationships, which allows for better modeling of complex relationships in stock markets. A third important factor is that the transformer model is relatively new in stock market prediction, indicating its potential for achieving more successful forecasts. The proposed transformer model was used to predict the closing values of the S&P 500, HSI, and Nikkei indices, and its performance was compared with traditional deep learning methods such as RNN, LSTM, and CNN regarding returns and statistical metrics. The experiments revealed that the transformer outperformed other models in predicting the closing prices of stock market indices. Moreover, when evaluating the models’ performances in terms of returns, similar results were obtained, indicating that the transformer model yielded higher returns. However, it was noted that this study had various limitations, such as focusing on a single stock market index and not considering the relationships among global financial markets. Future research should overcome these limitations and explore the applications of the transformer in other financial markets.

Lv et al. (2022) highlighted the inadequacy of traditional forecasting models in predicting stock market indices, particularly noting that the noise in financial time series adversely affects the model’s predictive performance. In this regard, they conducted detailed research on deep learning methods to successfully predict the closing prices of stock market indices, proposing a hybrid prediction model based on CEEMDAN-DAE-LSTM. This proposed model addresses the complexity and noise of stock market index data and consists of three stages. Firstly, the complete ensemble empirical mode decomposition with adaptive noise (CEEMDAN) approach was applied to the closing price data of stock market indices to decompose the data into a series of intrinsic mode functions (IMFs), resulting in a less noisy and more stable representation. In the second stage, the deep autoencoder (DAE) method was used to extract deep features and remove irrelevant information, while in the final stage, the prediction process was performed using the LSTM method, a deep learning approach. To evaluate the prediction performance of the CEEMDAN-DAE-LSTM model, six datasets consisting of the closing prices of stock market indices, including the Shanghai Composite Index (SH), Shenzhen Stock Exchange Index (SZ), HSI, Nikkei 225, DJI, and S&P 500, were utilized. Additionally, the performance of the proposed model was compared with five different prediction models, namely Single LSTM, Single RNN, EMD-DAE-LSTM, CEEMDAN-PCA-RNN, and CEEMDAN-PCA-LSTM. Experimental results demonstrate that the proposed model outperforms other models on these various stock market indices, improving prediction accuracy. The findings indicate that the CEEMDAN-DAE-LSTM model combines the advantages of CEEMDAN, DAE, and LSTM methods to provide a more effective prediction capability. To guide future research, it is suggested that macroeconomic variables and factors such as news sentiment be added to the dataset to enhance diversity and individual improvements for each proposed module to improve the model’s prediction capability.

Shah et al. (2022) proposed a deep learning-based hybrid model consisting of CNN and LSTM methods to predict the closing price of the Nifty 50 stock market index. For the feature set of the proposed model, in addition to the raw price data of the index, technical indicators, foreign indices, exchange rates, and commodity price data were utilized, resulting in a total of 48 features. The CNN method was employed to extract high-level features from these obtained features, while the LSTM method was applied to predict the next-day value of the Nifty 50 index. The proposed model achieved a MAPE rate of 2.54% on the training dataset, representing a significant improvement compared to similar studies. Additionally, the proposed CNN-LSTM model was compared with the traditional buy-and-hold strategy. With the proposed model, a return of 342% was achieved in 10 years for the Nifty 50 index, while the traditional buy-and-hold strategy yielded a return of only 107%. This indicates the superiority of the CNN-LSTM model in terms of returns compared to the traditional buy-and-hold strategy. It is noted that future research will focus on conducting more detailed investigations to better adapt the prediction model to noise and random events.

In their study, Lawi, Mesra & Amir (2022) created and evaluated eight new architectural models to predict the stock prices of AMZN, GOOGL, BLL, and QCOM. These models combined the LSTM and GRU models with a four-neural network block architecture to identify joint movement patterns in the stock market using time series data. Therefore, four different LSTM/GRU model architectures for stock price prediction were proposed: the direct model, downsizing model, tuned downsizing model, and stabilized downsizing model. These models used differently processed output shapes to predict stock prices. The proposed eight models were evaluated using three accuracy measures, namely MAPE, root mean squared prediction error (RMSPE), and rooted mean dimensional percentage error (RMDPE), and upper, average, and lower accuracy values were obtained for each. The findings showed that GRU called direct model (Model-1) provided the highest training and test data accuracy.

Based on literature reviews conducted by Chen, Wu & Wu (2022), it has been observed that satisfactory prediction performance has been achieved with deep learning-based models in the scope of stock prediction. However, it is noteworthy that most of the proposed models in these studies used data from a single stock. Additionally, it has been observed that the lack of consideration for the influence of similar stocks within the same group negatively affects the long-term prediction performance. Based on the findings of these studies, a new hybrid model based on deep learning was proposed to improve prediction performance. In the proposed KD-LSTM model, 16 bank stocks with similar trends listed on the Chinese stock market were clustered using the k-means method with dynamic time warping (DTW) distance metric. The value of k was set between 2 and 5 during clustering, and based on the clustering results, the data of four bank stocks identified to belong to the same cluster each time were used to train the LSTM model. Experimental results reported that the clustering approach used in the prediction model positively affected the prediction performance.

Gupta, Bhattacharjee & Bishnu (2022) proposed a new model called StockNet, based on a GRU, to predict the CNX Nifty index’s opening price and overcome the overfitting problem. They introduced a novel data augmentation approach with their proposed model. The StockNet model consists of two parallel modules: an injection module to address the overfitting issue and an investigation module for predicting the index value. Due to the limited amount of data available for the proposed model, overfitting became a challenge in training deep-learning models with such limited data. To mitigate this issue, they proposed a GRU-based data augmentation approach. During the data augmentation process, they considered ten stocks highly correlated with the stock index and explored combinations of these ten stocks in the injection module. To evaluate the performance of the proposed StockNet model, both the real dataset of the CNX Nifty 50 index and the synthetic dataset were used, and comparisons were made with six different prediction models, including DNN and RNN. The comparisons concluded that StockNet exhibited the best performance among the six models.

Polamuri, Srinivas & Mohan (2022) noted the increasing significance of generative adversarial networks (GAN) in recent years, particularly in computer vision. However, they observed that GAN was not widely used for stock market prediction due to the challenging process of hyperparameter tuning. Taking this as their primary motivation, Polamuri, Srinivas & Mohan (2022) proposed a hybrid forecasting framework utilizing GAN to perform stock market prediction. In the proposed model, LSTM and CNN models were used for the two essential components of GAN, namely the generator and the discriminator, respectively. Additionally, reinforcement learning and Bayesian optimization were employed to overcome the difficulty of hyperparameter tuning in the GAN model. The proposed hybrid model also incorporates feature extraction, feature selection, and dimensionality reduction approaches for data preprocessing. An autoencoder was utilized for feature extraction from stock market data, Extreme Gradient Boosting (XGBoost) was employed for filtering features based on their importance, and PCA was used for dimensionality reduction. After the data preprocessing step, the prediction process was carried out using the GAN model. While the proposed model achieved satisfactory performance, it is noteworthy that the computational cost of the model was quite high.

Akşehir & Kiliç (2022) have noted through their literature review that the CNN model has been successfully applied in stock prediction problems. However, they observed data imbalance problems in studies where stocks’ next-day trade action (buy/sell/hold) was predicted using a 2D-CNN model. They emphasized that the labeling approach was the main factor in this problem. In this regard, they proposed a new rule-based labeling approach to address the data imbalance problem. To investigate the impact of this proposed labeling approach on model performance, they predicted the next-day trade actions of stocks in the Dow30 index. For this purpose, the historical price data of stocks were obtained from Yahoo Finance, and each trading day was labeled using the proposed labeling approach. Subsequently, input variables that could positively influence the model’s prediction performance were determined. The most commonly used 15 technical indicators in the literature, along with external factors such as gold and oil prices, were considered for this purpose. Additionally, a correlation-based feature selection method was applied to these variables. Six different input variable sets were created based on both the feature selection approach and the information obtained from the literature review. These input variable sets were transformed into images to train the 2D-CNN model. Both traditional and sliding window training-test approaches were applied during the model training process, and the model’s performance was compared with other CNN-based prediction models in the literature. Experimental results demonstrated that the proposed labeling approach effectively addressed the data imbalance problem. Furthermore, it was observed that the CNN prediction model with the proposed feature selection and labeling methods achieved a 3–22% higher accuracy rate than other CNN-based models in previous studies.

He, Siu & Si (2023) noted that deep learning models are commonly used for stock direction prediction, but the performance of these models could be negatively affected, especially for newly publicly offered stocks, due to the scarcity of historical price data. To address this issue, they proposed an example-based deep transfer learning model (IDTLA) equipped with an attention mechanism. The proposed model utilized a deep transfer learning approach to find effective ways of learning from limited training data. For stock direction prediction, new instances were first created using the IDTLA architecture, and then the entire dataset was trained with the LSTM model.

Chen & Zhu (2023) pointed out that while various artificial intelligence algorithms are used to create prediction models for financial market forecasting, evaluating these models often focuses on accurate price prediction. They focused on determining buy-sell points to achieve high and consistent profits and proposed an effective method. This proposed method consists of piecewise linear representation (PLR), CNN, and LSTM approaches, named PLR-CNN-LSTM. Data from various stocks belonging to companies in Turkey and the United States were considered to evaluate the performance of the PLR-CNN-LSTM model, and historical price data for these stocks were gathered. Subsequently, 15 technical indicator values were calculated using this price data, and a dataset was created. After dataset creation, the PLR method was used to label buy/sell/hold points and identify turning points. Then, considering period values ranging from 3 to 23 for each technical indicator, two-dimensional image representations were created to obtain 20x15 images. These images were fed into the CNN-LSTM model to predict future stock buy-sell signals. Comparisons were made with the PLR-CNN-TA and PLR-LSTM models to evaluate the performance of the proposed PLR-CNN-LSTM model. The comparisons revealed that the proposed PLR-CNN-LSTM model made more successful predictions, resulting in higher profits. However, the main problem here is that after labeling, there is more hold-labeled data than buy/sell-labeled data, making it difficult to differentiate between buy-sell signals. Therefore, this situation also affects the performance of the prediction model.

Mu et al. (2023) combined two data types influencing stock closing prices and proposed the MS-SSA-LSTM hybrid model for predicting these prices. In this proposed hybrid model, comments related to stocks were first collected, and sentiment analysis was performed to obtain a sentiment score. Then, the historical price data of stocks and sentiment index were combined and fed into an LSTM model optimized with the sparrow search algorithm (SSA). The proposed MS-SSA-LSTM model was applied to six different stocks in the Chinese market. Additionally, six other models were created to investigate the effect of each module, including multiple data sources and SSA-optimized LSTM, on the model. Experimental results showed that the MS-SSA-LSTM model made closer predictions to the stock closing price. Additionally, it was observed that using multi-source data and SSA for hyperparameter tuning positively influenced the prediction performance of the stock prediction model.

Zhang, Ye & Lai (2023) stated that various prediction methods ranging from traditional time series techniques to machine learning-based models have been proposed for stock index prediction, achieving a certain level of accuracy with these prediction models. In this direction, they proposed the CNN-BiLSTM-attention hybrid model to improve the accuracy of stock index prediction. In this model, CNN was used to extract temporal features of time series data, followed by BiLSTM to learn dynamic change patterns from these features. Additionally, an attention mechanism was applied to the extracted features to automatically assign weights, thereby reducing the influence of irrelevant information and exploring deeper temporal correlations. Subsequently, the closing value of the stock index was predicted using a dense layer. The proposed CNN-BiLSTM-attention model was first applied to predict the closing value of the CSI 300 index and compared with LSTM, CNN-LSTM, and CNN-LSTM-attention prediction models. Experimental results showed that the proposed hybrid model outperformed the other three models, thus making close predictions of the closing value of the CSI 300 index. To confirm the prediction stability and robustness of the model, experiments were conducted on 11 stock indices, including three Chinese and eight international stock indices. The results indicated that the proposed model effectively predicted both Chinese and other countries’ stock indices and possessed a certain degree of generalization. Additionally, Zhang, Ye & Lai (2023) stated that this study relied on stock indices’ price data, but many factors influence stocks or indices. Therefore, it was noted that the proposed model has structural limitations. In this regard, it was suggested that various information collected from different sources related to stock prices be integrated into the prediction model to improve prediction accuracy.

Cagliero, Fior & Garza (2023) highlighted the increasing interest in machine learning-based trading systems utilizing stock market data and information provided by candlestick patterns. However, they pointed out various disadvantages of these developed models. Firstly, machine learning models tend to generate many buy/sell signals, leading to a high false positive rate. Secondly, models trained on datasets created from candlestick formations and price data face a dimensionality problem. This study proposed separating the machine learning and pattern recognition steps to overcome these disadvantages and create a short-term stock trading system. The proposed model primarily focused on various machine learning models, such as MLP, SVM, RF, LSTM, etc., to predict the direction of stocks for the next day. A pattern-based filtering process was conducted in the pattern recognition part, considering pattern features such as confidence level and freshness. Then, the proposed pattern recognition approach was used to prioritize the recommendations of machine learning models and verify their reliability. Three different agreement strategies were determined by looking at the suggestions of the two methods. This proposed model was applied to stocks in the S&P 500 and FTSE MIB 40 indices. It was observed that separately addressing machine learning methods and pattern recognition positively influenced the trading strategy.

Kim et al. (2023) conducted a study focusing on predicting the direction of the KOSPI 200 index and identifying the features the model emphasized during this prediction. Additionally, a trading simulation was conducted using the identified features. For the proposed model, firstly, the 30-minute data of the KOSPI 200 index was collected, and direction labeling was performed based on consecutive data. Subsequently, 16 technical indicators were considered, and 16x16 images were obtained by considering 16-period values starting from 7 and increasing by three units up to 52. The CNN model was trained on the generated image dataset. Then, to confirm which technical indicators or features the model focused on during direction prediction, the gradient-weighted class activation mapping (Grad-CAM) method was applied. Trading simulations were conducted using the important features identified by the Grad-CAM method. The proposed trading strategy was compared with various strategies, such as a simple buy-and-hold strategy and a strategy based on the most commonly used buy/sell technical indicators. Experimental results demonstrated that the proposed strategy yielded higher returns compared to others.

Qi, Ren & Su (2023) proposed a hybrid forecasting model for stock index prediction consisting of GRU, CEEMDAN, and wavelet transform. CEEMDAN and wavelet transform methods were used to remove noise from the index data, while GRU was utilized to predict the next day’s index value. The stock index data was first decomposed into IMFs using the CEEMDAN method in the proposed denoising approach. Despite containing some helpful information, the IMF with high-frequency components also contained more noise. Therefore, the noise was removed by applying wavelet transform instead of directly discarding these components. After denoising the stock index data using the CEEMDAN-wavelet transform approach, the GRU model was trained on the denoised data for prediction. To evaluate the performance of the GRU based on the CEEMDAN-wavelet hybrid model, S&P 500 and CSI 300 index data were used, and performance comparisons were made with GRU, LSTM, ARIMA, CNN-BiLSTM, and ANN models. Experimental results demonstrated that the proposed model outperformed traditional models in making predictions. However, challenges such as the influence of human factors on financial markets and the inability to model emotional factors exist. Therefore, future research may consider methods such as news analysis and sentiment analysis to enhance the model’s effectiveness.

Yao, Zhang & Zhao (2023) emphasized the complexity of modeling and predicting stock market indexes, highlighting the inadequacy of existing prediction models in the literature. To overcome this challenge, they proposed a hybrid model called MEMD-TCN based on multivariate empirical mode decomposition (MEMD) and temporal convolutional networks (TCN). In the proposed model, the COHLV stock index data, encompassing closing price, opening price, highest price, lowest price, and trading volume, were initially decomposed into IMFs using MEMD. Subseries were then obtained for each feature. Then, subseries of the same frequency were fed as input to the TCN network. Finally, the predicted results of all subseries were combined to obtain the closing values of the stock indexes for the next day. Data from seven stock market indexes in China, the United States, Europe, and the Asia-Pacific region were used to evaluate the performance of the proposed MEMD-TCN model. Additionally, the model’s prediction performance was compared with 14 models, including traditional econometric, machine learning, and hybrid models. The experiments demonstrated that the proposed MEMD-TCN model outperformed all other benchmark models regarding prediction performance. Moreover, it was observed that combining different decomposition algorithms with the TCN model further improved prediction performance. Furthermore, it was stated that this study provides a general model that can be used not only for stock market indexes but also for other research areas.

Zhao & Yang (2023) conducted a study addressing the challenge of predicting stock price directions due to the characteristics of stock price data. They proposed a new prediction framework called SA-DLSTM by combining sentiment analysis, denoising autoencoder, and LSTM model. For their proposed model, they collected price data related to the HSI index and textual data from various forum websites associated with the index. They first used the denoising autoencoder method to extract features from the price data, obtaining features strongly correlated with price data while effectively removing noise. Then, they performed sentiment analysis on the collected textual data using the emotion-enhanced CNN (ECNN) method to obtain a sentiment index. The features extracted from the stock price and sentiment index data were then fed into an LSTM network for stock price direction prediction. To evaluate the performance of the proposed SA-DLSTM model, it was compared with traditional machine learning and statistical methods. Additionally, trading simulations were conducted to investigate the model’s impact on profitability. The experimental results demonstrated that the SA-DLSTM model achieved the highest prediction accuracy and captured suitable trading points (buy/sell signals), resulting in high returns.

Jarrah & Derbali (2023) proposed a deep learning-based prediction model to predict the weekly closing prices of three stocks in the Saudi Stock Market Index: Mobily, STC, and Zain. Their study preferred the LSTM method from deep learning techniques and compared the performance of both single-variable and multi-variable LSTM prediction models. For the proposed prediction models, they first removed noise from the stock price data using the exponential smoothing (ES) approach. Then, for single-variable analysis, only the closing price data were used, while for multi-variable analysis, the closing, opening, highest, and lowest price data were inputted into the LSTM model to predict the weekly closing values of the stocks. The prediction results of both models were evaluated using metrics such as MAE, MSE, RMSE, and MAPE. The evaluations revealed that the multi-variable model made more accurate predictions than the single-variable model. The results highlight the effectiveness of multi-variable models and the importance of noise reduction approaches in stock price prediction. Furthermore, the authors emphasized the need for future studies to focus on making longer-term predictions and examining the impact of different economic factors.

Wang & Zhu (2023a) identified two main shortcomings in decomposition-integration-based prediction models for stock price prediction after conducting literature research. First, in decomposition-based models, only the closing price of the stock data is usually considered, while other factors influencing the stock are ignored. Second, prediction results are linearly combined after training the separately obtained sub-series resulting from decomposition. To address these shortcomings, they proposed a new prediction model using the idea of adding effective influencing factors and utilizing classification prediction. The proposed multi-factor two-stage deep integration model for predicting stock index closing prices consists of four stages: multi-factor analysis, feature clustering, classification prediction, and nonlinear integration. In the first stage, the most important factors influencing stock prices were determined using the XGBoost method in the multi-factor analysis module, considering both basic factors such as opening price, highest price, lowest price, etc., and non-basic factors such as oil price, interest rate, gold price, exchange rate, consumer confidence index, etc. Then, the dataset containing these features was divided into train and test datasets. In the second stage, feature clustering was performed using the k-means method on the training dataset, grouping similar data to facilitate the model’s learning process and improve the accuracy of predictions. In the classification prediction stage, an optimized LSTM model with a genetic algorithm was trained separately on each cluster obtained from clustering. Finally, the prediction results obtained in the previous stage were combined nonlinearly in the nonlinear integration module. The proposed model was used to predict the closing prices of the Shanghai Stock Exchange Composite Index, Shenzhen Stock Exchange Component Index, and New York Stock Exchange Composite Index. Additionally, comparisons were made with single LSTM, EMD-LSTM, CEEMDAN-LSTM, and VMD-LSTM models to evaluate the model’s effectiveness. Experimental results showed that the proposed model outperformed the other models in all indices. In future studies, the proposed model will be further examined for stock direction prediction and applied to other fields, such as the oil and exchange markets.